Explanatory Notes to Legislative Proposals Relating to the Income Tax Act and Regulations (Technical Amendments)

Preface

These explanatory notes are provided to assist in an understanding of legislative proposals relating to the Income Tax Act and Income Tax Regulations. These explanatory notes describe the proposed amendments, clause by clause, for the assistance of Members of Parliament, taxpayers and their professional advisors.

The Honourable Chrystia Freeland, P.C., M.P.,

Deupty Prime Minister and Minister of Finance

These notes are intended for information purposes only and should not be construed as an official interpretation of the provisions they describe.

Table of Contents

| Clause in Legislative Proposals | Section Amended | Topic |

|---|---|---|

| Legislative Proposals Relating to Income Tax | ||

| Income Tax Act | ||

| 1 | 8 | Deductions |

| 2 | 12 | Inclusions |

| 3 | 13 | Definitions |

| 4 | 15 | Shareholder debt |

| 5 | 18.2 | Definitions |

| 6 | 56 | Amounts to be included in income for year |

| 7 | 62 | Moving expenses of students |

| 8 | 66.7 | Change of control |

| 9 | 81 | Ship of resident corporations - gains |

| 10 | 87 | Public corporation |

| 11 | 95 | Definitions for this Subdivision |

| 12 | 104 | Reference to trust or estate |

| 13 | 107.4 | Application of paragraph (1)(a) |

| 14 | 110 | Employee options |

| 15 | 110.6 | Definitions - "qualified small business corporation share" |

| 16 | 112 | Loss on share held by trust |

| 17 | 115 | Non-resident persons — 2010 Olympic and Paralympic Winter Games |

| 18 | 117.1 | Annual adjustment |

| 19 | 118 | Definitions - "pension income" |

| 20 | 120.4 | Definitions - "excluded amount" |

| 21 | 122.91 | Training amount limit |

| 22 | 126 | Former resident — deduction |

| 23 | 127.42 | Deemed rebate in respect of fuel charges |

| 24 | 127.52 | Adjusted taxable income determined |

| 25 | 128.1 | Post-emigration loss — reassessment period |

| 26 | 146 | Registered Retirement Savings Plans |

| 27 | 146.3 | Registered Retirement Income Funds |

| 28 | 146.5 | Advanced Life Deferred Annuity |

| 29 | 146.6 | First Home Savings Account |

| 30 | 147 | Definitions - "deferred profit sharing plan" |

| 31 | 147.1 | Notice of revocation |

| 32 | 147.4 | RPP annuity contract |

| 33 | 149.1 | Exclusions |

| 34 | 150 | Returns |

| 35 | 152 | Assessment |

| 36 | 153 | Withholding |

| 37 | 160.1 | Where excess refunded |

| 38 | 160.2 | Rules applicable |

| 39 | 163 | Repeated failure to report income |

| 40 | 164 | Refunds |

| 41 | 169 | Disposition of appeal on consent |

| 42 | 183.3 | Tax on Repurchases of Equity |

| 43 | 183.4 | Return |

| 44 | 188 | Revocation tax |

| 45 | 205 | Definitions - "excess ALDA transfer" |

| 46 | 207.04 | Both prohibited and non-qualified investment |

| 47 | 207.5 | Definitions |

| 48 | 211.8 | Disposition of approved share |

| 49 | 212 | Tax |

| 50 | 212.1 | Trusts and partnerships look-through rule |

| 51 | 214 | Standby charges and guarantee fees |

| 52 | 215 | Withholding and remittance of tax |

| 53 | 220 | Date of late election, amended election or revocation |

| 54 | 222 | Limitation period restarted |

| 55 | 241 | Provision of information |

| 56 | 248 | Definitions |

| 57 | 260 | Non-disposition |

| Income Tax Regulations | ||

| 58 | ITR 204.2 | Additional Reporting - Trusts |

| 59 | ITR 600 | Elections |

| 60 | ITR 1000 | Property Dispositions |

| 61 | ITR 1000.1 | Realization of Options |

| 62 | ITR 1101 | Businesses and Properties |

| 63 | ITR 1400 | Non-Life Insurance Business |

| 64 | ITR 2301 | Principal Residences |

| 65 | ITR 4301 | Prescribed Rate of Interest |

| 66 | ITR 5600 | Prescribed Distributions |

| 67 | ITR 5907 | Interpretation |

| 68 | ITR 6400 | Child Tax Credits |

| 69 | ITR 6701 | Prescribed Venture Capital Corporations, Labour sponsored Venture Capital Corporations, Investment Contract Corporations, Qualifying Corporations and Prescribed Stock Savings Plans |

| 70 | ITR 6702 | Prescribed Venture Capital Corporations, Labour sponsored Venture Capital Corporations, Investment Contract Corporations, Qualifying Corporations and Prescribed Stock Savings Plans |

| 71 | ITR 6802 | Prescribed plan or arrangement |

| 72 | ITR 8308 | Conditions — Retroactive Contributions |

| 73 | ITR 8502 | Permissible Contributions |

| 74 | ITR 8503 | Defined Benefit Provisions |

| 75 | ITR 8506 | Money Purchase Provisions |

| 76 | ITR 8512 | Registration and Amendment |

| 77 | ITR 8513 | Designated laws |

| 78 | ITR 9002 | Prescribed Property not Mark-to-Market Property |

Income Tax Act

Clause 1

Expenses of railway employees

Income Tax Act (the Act or ITA)

8(1)(e)

Paragraph 8(1)(e) permits a railway employee to deduct amounts expended for the purpose of earning income from employment in respect of meals and lodging under certain circumstances. The deduction of an amount under this provision is only allowed to the extent that the employee was not reimbursed and was not entitled to be reimbursed for the amount.

Paragraph 8(1)(e) is amended to provide that no deduction is allowed for an amount in respect of which the employee received a non-taxable allowance or is entitled to receive such an allowance.

Transport employee's expenses

ITA

8(1)(g)

Paragraph 8(1)(g) permits a transport employee to deduct amounts expended for the purpose of earning income from employment in respect of meals, lodging and travel under certain circumstances. The deduction of an amount under this provision is only allowed to the extent that the employee was not reimbursed and was not entitled to be reimbursed for the amount.

Paragraph 8(1)(g) is amended to provide that no deduction is allowed for an amount in respect of which the employee received a non-taxable allowance or is entitled to receive such an allowance.

Also, the French version of paragraph 8(1)(g) is amended to better align the English and French versions.

Clause 2

Refunds

ITA

12(1)(z.6)

Paragraph 12(1)(z.6) requires the inclusion in income of any amount received by the taxpayer in the year in respect of a refund of an amount that was deducted under paragraph 20(1)(vv) in computing income for any taxation year.

The French version of paragraph 12(1)(z.6) is amended to better align the English and French versions.

Definition of flipped property

ITA

12(13)(b)(i.1)

Subsection 12(13) of the Act provides the definition of "flipped property" of a taxpayer. Paragraph 12(13)(b) provides exclusions to the definition of "flipped property" in certain circumstances. For example, subparagraph 12(13)(b)(i) provides an exclusion for property owned by the taxpayer for less than 365 consequence days prior to its disposition where the disposition can reasonably be considered to occur due to, or in anticipation of, the death of the taxpayer or a person related to the taxpayer.

Under existing paragraph 12(13)(b), where the taxpayer is a trust, a deemed disposition by the taxpayer as a consequence of paragraph 104(4)(a) of the Act would be captured by the definition of "flipped property". A beneficiary under a trust is not related to the trust. The death of the beneficiary, whose death triggers the deemed disposition under paragraph 104(4)(a), is not the death of a person related to the taxpayer, and therefore does not trigger the exclusion provided in subparagraph 12(13)(b)(i).

Paragraph 12(13)(b) is amended to add an exclusion in new subparagraph 12(13)(b)(i.1) for a deemed disposition by a trust as a consequence of paragraph 104(4)(a).

This amendment applies in respect of dispositions that occur on or after January 1, 2023.

Clause 3

Definitions

ITA

13(21)

French Definition - "fraction non amortie du coût en capital"

Subsection 13(21) contains a number of definitions, including the definition "undepreciated capital cost", that apply for purposes of section 13. The definition "undepreciated capital cost" in that subsection also applies for purposes of the Act by operation of subsection 248(1).

The undepreciated capital cost to a taxpayer of depreciable property of a prescribed class as of any time means the amount determined by the formula in that definition.

The French version of the description of E in that formula is amended to better align the English and French versions.

Clause 4

Shareholder debt

ITA

15(2)

Subsection 15(2) requires that certain indebtedness be included in the income of the debtor in the year in which the indebtedness arose. This subsection is intended to prevent a debtor, that is directly or indirectly a shareholder of a particular corporation or that is connected with a shareholder of the particular corporation, from avoiding tax by receiving property from the corporation through an otherwise non-taxable loan, rather than as a dividend or other taxable amount.

Certain debtors are excluded from the application of subsection 15(2), including a corporation resident in Canada (CRIC) and a partnership, each member of which is a CRIC. Subsection 15(2) is amended to relocate these exclusions to new subsection 15(2.01) following the addition of a new exception for tiered partnerships in new paragraph 15(2.01)(b). See the commentary to subsection 15(2.01) for more information.

This amendment applies to loans received and indebtedness incurred after October 31, 2011.

Excluded persons and partnerships

ITA

15(2.01)

Subsection 15(2) requires that certain indebtedness be included in the income of the debtor in the year in which the indebtedness arose. Certain debtors are currently excluded from the application of subsection 15(2), including a corporation resident in Canada (CRIC) and a partnership, each member of which is a CRIC. Subsection 15(2) is not intended to apply to loans received by a partnership, that is held directly or indirectly, solely by CRICs.

New subsection 15(2.01) is established to compile a list of debtors to which subsection 15(2) does not apply. These debtors are:

- CRICs; and

- partnerships, each member of which is either a CRIC, or another partnership described here (to accommodate tiered-partnership structures).

Consequently, subsection 15(2) will not apply to a partnership if all the members are, directly or indirectly (through one or more other partnerships), CRICs.

Example – tiered-partnership structure

Relevant facts:

- two CRICs (Canco1 and Canco2) are the only members of a foreign partnership (Foreign LP1);

- Canco1 and Foreign LP1 are the only members of another foreign partnership (Foreign LP2);

- Foreign LP2 wholly owns a foreign corporation (FA); and

- Canco2 makes a loan to Foreign LP2 in the year.

Tiered-partnership structure

Since Foreign LP2 is a shareholder of a particular corporation (FA), and Foreign LP2 has received a loan from a corporation related to FA (Canco2), in the absence of new subsection 15(2.01), subsection 15(2) would apply to include the amount of the loan in computing the income of Foreign LP2 for the year.

However, Foreign LP2 is a partnership described in new paragraph 15(2.01)(b) because each member of the partnership is a CRIC (Canco1) or another partnership described in paragraph (b) (Foreign LP1). Foreign LP1 is a partnership described in paragraph (b) because each member is a CRIC (Canco1 and Canco2). Consequently, subsection 15(2) does not apply to the loan from Canco2 to Foreign LP2.

Subsection 15(2.1) was previously amended (with effect as of October 31, 2011) to clarify that a partnership can be connected with a shareholder of a particular corporation if that partnership does not deal at arm's length with, or is affiliated with, the shareholder. Consequently, this amendment applies to loans received and indebtedness incurred after October 31, 2011 to likewise clarify that subsection 15(2) does not apply to a partnership, all of whose members are CRICs or other partnerships described in new paragraph 15(2.01)(b).

Additionally, subsection 15(2) may unintentionally impact certain debtors belonging to the same foreign affiliate group as the particular corporation (referred to in subsection 15(2)). To address this concern, paragraph 15(2.01)(a) is amended (applicable to loans received or indebtedness incurred after Announcement Date) to exclude from the application of subsection 15(2), a debtor that is

- a foreign affiliate of the particular corporation; or

- a foreign affiliate of a person resident in Canada with which the particular corporation does not deal at arm's length.

As a consequence of these amendments, subsection 15(2) will not apply to loans made to partnerships provided that all of their members are the above-described foreign affiliates, CRICs, or other partnerships described in paragraph 15(2.01)(b).

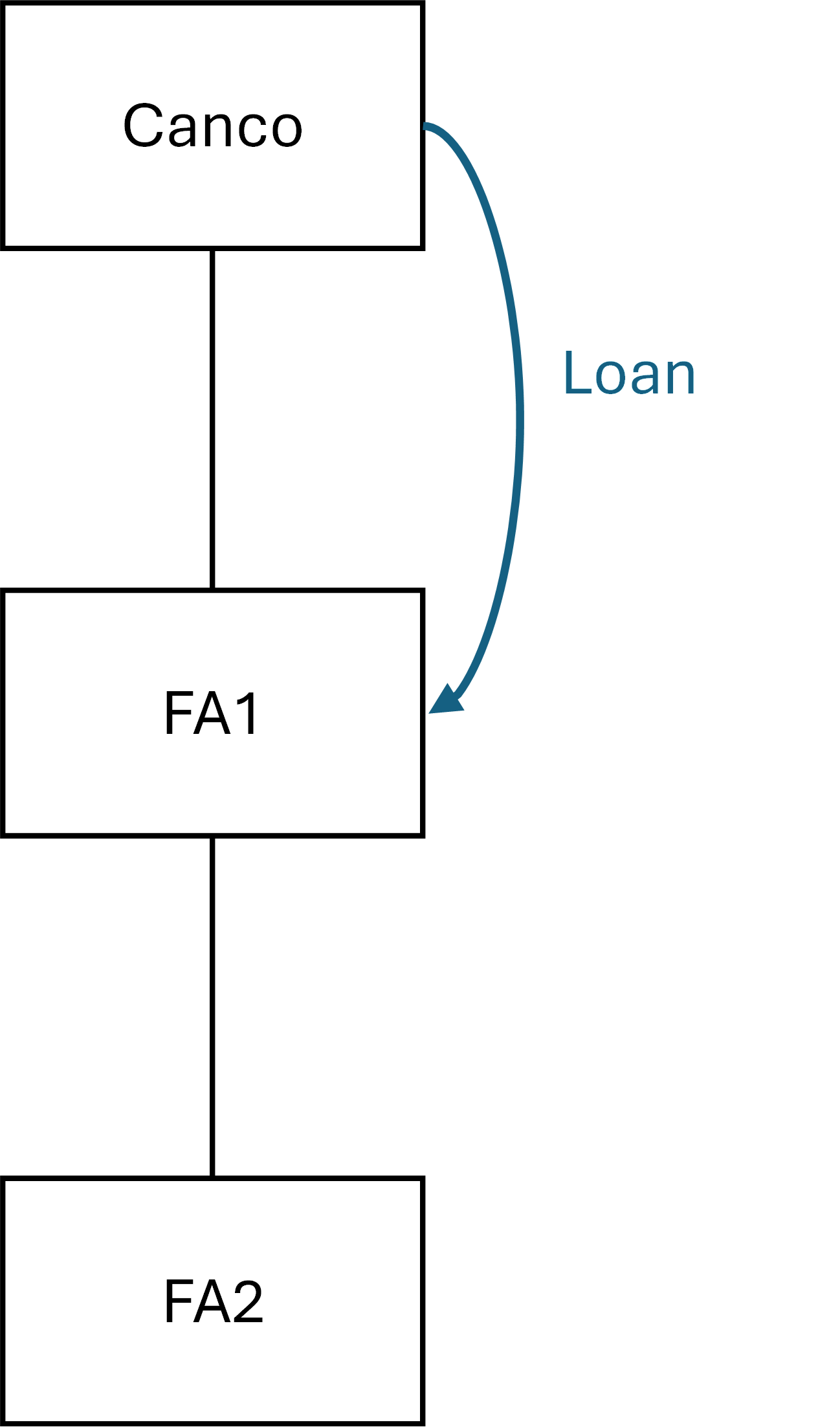

Example – tiered-foreign affiliate structure

Relevant facts:

- a CRIC (Canco) wholly owns a foreign corporation (FA1);

- FA1 wholly owns another foreign corporation (FA2); and

- Canco makes a loan to FA1 in the year.

Tiered-foreign affiliate structure

Since FA1 is a shareholder of a particular corporation (FA2), and FA1 has received a loan from a corporation related to FA2 (Canco), in the absence of new subparagraph 15(2.01)(a)(iii), subsection 15(2) would apply to include the amount of the loan in computing the income of FA1 for the year.

However, FA1 is a foreign affiliate of a person resident in Canada with which FA2 does not deal at arm's length (Canco) as described in new subparagraph 15(2.01)(a)(iii). Consequently, subsection 15(2) does not apply to the loan from Canco to FA1.

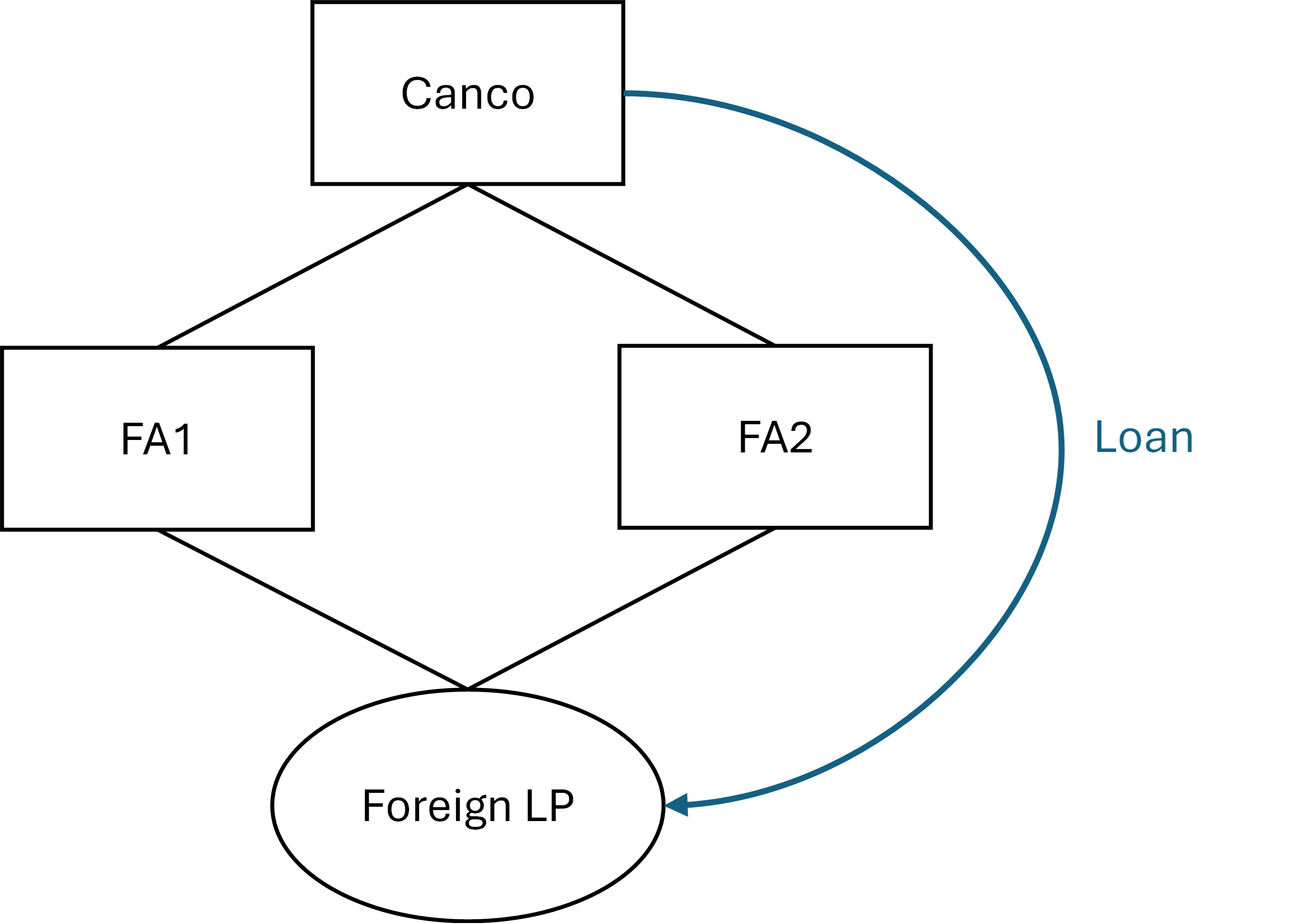

Example – partnership loan with foreign affiliate member

Relevant facts:

- a CRIC (Canco) wholly owns two foreign corporations (FA1 and FA2);

- FA1 and FA2 are the only members of a foreign partnership (Foreign LP); and

- Canco makes a loan to Foreign LP in the year.

Partnership loan with foreign affiliate member

Pursuant to subsection 15(2.1), Foreign LP is connected, in respect of a particular corporation (FA1), with a shareholder of FA1 (Canco) because Foreign LP is affiliated with Canco.

In the absence of new subparagraph 15(2.01)(a)(iii), since Foreign LP is connected with a shareholder of FA1 (Canco), and Foreign LP has received a loan from a corporation related to FA1 (Canco), subsection 15(2) would apply to include the amount of the loan in computing the income of Foreign LP for the year.

However, with new subparagraph 15(2.01)(a)(iii), Foreign LP is a partnership described in paragraph 15(2.01)(b) because each member of the partnership (FA1 and FA2) is a foreign affiliate of a person resident in Canada with which FA1 does not deal at arm's length (Canco). Consequently, subsection 15(2) does not apply to the loan from Canco to Foreign LP.

Similar results would apply if FA2 is the particular corporation.

This amendment applies to loans received and indebtedness incurred after Announcement Date.

Meaning of connected

ITA

15(2.1)

Subsection 15(2) requires that certain indebtedness be included in the income of the debtor in the year in which the indebtedness arose. Paragraphs 15(2)(a) to (c) describe the debtors to which this rule applies in terms of their relationship with a particular corporation. In particular, paragraph 15(2)(b) provides that subsection 15(2) may apply to a debtor that is connected with a shareholder of the particular corporation.

Subsection 15(2.1) specifies that a debtor is connected with the shareholder if the debtor does not deal at arm's length with or is affiliated with the shareholder, unless the debtor is

- a foreign affiliate of the particular corporation, or

- a foreign affiliate of a person resident in Canada with which the particular corporation does not deal at arm's length.

Subsection 15(2.1) is amended to remove its paragraphs (a) and (b) as a consequence to the inclusion of these exceptions and other new exceptions to subsection 15(2) in amended subsection 15(2.01). Consequently, the exception to subsection 15(2) for persons described in paragraphs 15(2.1)(a) and (b) is no longer restricted to the connected test described in subsection 15(2.1). See the commentary to subsection 15(2.01) for more information.

This amendment applies to loans received and indebtedness incurred after Announcement Date.

Clause 5

Definitions

ITA

18.2(1)

"excluded interest"

Paragraph (c) of the definition "excluded interest" is amended to expand the circumstances in which an excluded interest election is available in respect of interest paid or payable to a financial institution group entity. It has also been redrafted in parts for clarity.

As a result of the amendments to paragraph (c), where a payee is a financial institution group entity, an excluded interest election is permitted if the payer either is a financial institution group entity, or would be a "special purpose loss corporation" (as defined in subsection 18.2(1)) if the reference to "financial holding corporation" in that definition were replaced with a reference to "financial institution group entity".

This amendment is intended to facilitate loss utilization transactions that are effectively between financial institution group entities but that rely on the use of a temporary, intermediary special purpose loss corporation. As this loss entity is not itself a financial institution group entity, the excluded interest election would not otherwise be available where the loss entity pays interest to a financial institution group entity.

This amendment applies to taxation years of a taxpayer ending on or after Announcement Date.

"special purpose loss corporation"

The definition "special purpose loss corporation" is amended to clarify that the special purpose loss corporation's loss – the generation of which is the sole purpose for the special purpose loss corporation's existence – must derive from interest paid or payable to a financial holding corporation that is an eligible group entity in respect of the special purpose loss corporation, and must be used exclusively by a financial institution group entity that is an eligible group entity in respect of the special purpose loss corporation.

This amendment applies to taxation years of a taxpayer ending on or after Announcement Date.

Clause 6

Pension benefits, unemployment insurance benefits, etc.

ITA

56(1)(a)(i)

Subparagraph 56(1)(a)(i) includes in the income of a taxpayer for a year certain pension benefits received in the year.

Subparagraph 56(1)(a)(i) is amended by adding clause (H) to clarify that a transfer of unclaimed pension property from a registered pension plan to a designated entity (e.g., the Bank of Canada in the case of federally regulated pension plans) is not included in the income of an individual (i.e., neither the unlocatable former employee nor an unlocatable beneficiary) at the time of that transfer.

Subparagraph 56(1)(a)(i) is further amended by adding clause (C.2) to require that a payment from a designated entity to an eligible claimant must be included in the income of the claimant for the year it is so paid.

This amendment comes into force on royal assent.

Interest free or low interest loans

ITA

56(4.1)(c)

Subsection 56(4.1) applies in certain cases to attribute income from one individual ("the transferee") to another individual ("the transferor") with whom the transferee does not deal at arm's length.

The French version of paragraph 56(4.1)(c) is amended to better align the English and French versions.

Clause 7

Moving expenses of students

ITA

62(2)

Subsection 62(2) provides a deduction for the qualifying moving expenses of an individual who moves to or from Canada to pursue higher education.

The French version of subsection 62(2) is amended to better align the English and French versions.

Clause 8

Change of control

ITA

66.7(10)(j)(ii)(B)

Under subsection 66.7(10), a corporation is treated as a successor for the purposes of the successor rules in section 66.7 after an acquisition of control (or a change in the tax-exempt status) of the corporation.

The French version of clause 66.7(10)(j)(ii)(B) is amended to better align the English and French versions.

Clause 9

Ship of resident corporations - gains

ITA

81(1)(c.2)

Subsection 81(1) of the Act provides that certain amounts are not included in income and therefore are exempt from income tax. Paragraph 81(1)(c) provides a longstanding exemption for non-residents' international shipping income, and paragraph 81(1)(c.1) extends this exemption to certain Canadian-resident corporations.

A capital gain realized by a non-resident from the disposition of a ship used principally in international traffic (or personal or movable property pertaining to the ship's operation) is generally not subject to tax in Canada, because such a ship (or personal or moveable property) is not taxable Canadian property of the non-resident. To improve alignment between the treatment of the gains of non-residents and the gains of residents, new paragraph 81(1)(c.2) is added to exempt from tax the portion of a capital gain earned from the disposition of a ship (or personal or movable property pertaining to the ship's operation) that can reasonably be considered to have accrued while the ship was property of a corporation resident in Canada that can benefit from the exemption in paragraph 81(1)(c.1) and the ship was used by the corporation solely to earn income from international shipping.

This amendment applies to the portion of a taxable capital gain that accrues on or after December 31, 2023.

Clause 10

Public corporation

ITA

87(2)(ii)

Where there has been an amalgamation between two or more predecessor corporations after 1971, to which subsection 87(1) applies, and any of the predecessor corporations was a "public corporation" (as defined in subsection 89(1)) immediately before the amalgamation, paragraph 87(2)(ii) provides that the new corporation is deemed to have been a public corporation at the commencement of its first taxation year.

The definition "public corporation" in subsection 89(1) applies in determining whether a corporation resident in Canada is a public corporation for the purposes of the Act. A corporation is a "public corporation" at a particular time if it satisfies one or more of the criteria outlined in paragraphs (a) to (c) of the definition.

By virtue of paragraph (c) of the definition, once a corporation becomes a public corporation, it continues to be a public corporation if it is resident in Canada unless it complies with the prescribed conditions (subsection 4800(2) of the Income Tax Regulations) and either the corporation elects in a prescribed manner not to be a public corporation or the Minister designates the corporation not to be a public corporation.

However, even where the corporation complies with the prescribed conditions and an election or designation is made not to be a public corporation, it might still be a public corporation if a class of shares of the corporation is listed on a designated stock exchange (as defined in subsection 248(1)) in Canada by virtue of paragraph (a) of the definition. This result is problematic for certain acquisitions of publicly listed corporations since delays in the delisting process on certain stock exchanges can uphold the acquired corporation's status as a public corporation. If the acquired corporation is amalgamated with a private corporation, paragraph 87(2)(ii) will deem the new amalgamated corporation to be a public corporation.

To address this concern, paragraph 87(2)(ii) is amended by introducing an exception to the deeming rule that applies if:

- after the last time a class of shares of the predecessor corporation (that was a public corporation) became listed on a designated stock exchange in Canada and before the amalgamation, an election or designation was made in respect of the corporation under paragraph (c) of the "public corporation" definition;

- immediately before the amalgamation, the predecessor corporation was a subsidiary wholly-owned corporation (as defined in subsection 248(1)) of another corporation (other than a public corporation) (the "Parent"); and

- the amalgamation was a vertical amalgamation between the Parent and the predecessor corporation.

If these conditions are satisfied, the new corporation formed on the amalgamation will not be deemed to be a public corporation by virtue of paragraph 87(2)(ii).

This amendment is deemed to come into force on royal assent.

Clause 11

Definitions for this Subdivision

ITA

95(1)

The definition "foreign accrual property income" (FAPI) in subsection 95(1) of the Act is relevant for the purpose of determining amounts that a taxpayer is to include under subsection 91(1), as income from a share of a controlled foreign affiliate, in computing its income for a particular taxation year. It is also relevant for the purposes of determining the taxable surpluses and deficits of a foreign affiliate of a taxpayer. Variables A to C of the formula in the FAPI definition contain the additions to FAPI and variables D to H contain the deductions from FAPI.

Paragraph (b) of the description of A in the definition generally excludes from the FAPI of a foreign affiliate of a taxpayer dividends received from another foreign affiliate of the taxpayer. However, where a foreign affiliate receives an inter-affiliate dividend that is deductible for foreign tax purposes, the dividend is included in the recipient affiliate's FAPI, consistent with Recommendation 2.1 of the report under Action 2 of the Group of 20 and Organisation for Economic Co-operation and Development's Base Erosion and Profit Shifting Project (the "BEPS Action 2 report"), titled Final Report on Neutralising the Effects of Hybrid Mismatch Arrangements.

Paragraph (b) of the description of A in the FAPI definition is amended to no longer apply the deductible dividend test under subsection 113(5). Instead, the amended paragraph (b) applies a test using the various rules and definitions used for applying subsection 12.7(3), the secondary operative rule of the hybrid mismatch rules.

The amended paragraph (b) excludes inter-affiliate dividends from FAPI in two circumstances. The first exclusion is provided in subparagraph (i), which excludes from FAPI any dividends received from another affiliate where the recipient affiliate and the payor affiliate are resident in the same country. This exclusion applies regardless of whether the dividend is deductible for foreign tax purposes, so long as the residency test is met.

The second exclusion, which is in subparagraph (ii), applies to the extent a dividend does not result in a "deduction/non-inclusion mismatch" (as determined under paragraph 18.4(7)(c)). It limits the FAPI inclusion to circumstances where a dividend is deductible for foreign tax purposes but is not included in computing foreign relevant income or profits. If all or any portion of the amount of the dividend was deductible by the payor affiliate but not included in computing the "foreign ordinary income" (as defined in subsection 18.4(1)) of the recipient affiliate, there is an inclusion in the FAPI of the recipient affiliate to the extent of the amount of the deduction/non-inclusion mismatch. For this purpose, clauses (b)(ii)(A) and (B) set out two modifications in applying the deduction/non-inclusion mismatch test under subsection 18.4(6). First, that test is limited exclusively to the test in paragraph (b) of that subsection and thus ignores any inclusion of the dividend in "Canadian ordinary income". Absent this modification, there is a potential circularity as sub-clause 95(2)(f.11)(ii)(F)(IV) modifies the "Canadian ordinary income" definition to read in paragraph (b) of the FAPI definition. The second modification is made to the description of C in the definition "foreign ordinary income", to ensure that an inclusion in foreign ordinary income as a result of a "foreign hybrid mismatch rule" (as defined in subsection 18.4(1)) is taken into consideration in determining whether there is a deduction/non-inclusion mismatch.

Variable H in the FAPI definition is relevant where a foreign affiliate of a taxpayer is a member of a partnership that receives a dividend from another foreign affiliate of the taxpayer. It ensures that the dividend is not included in the member's FAPI. Variable H is amended to implement the same policy, and achieve a similar result, as the amendment to paragraph (b) of the description of A (described above).

These amendments apply in respect of dividends received on or after July 1, 2024.

Clause 12

Reference to trust or estate

ITA

104(1)

Subsection 104(1) provides a rule under which a reference to a trust or estate is read in the Act as a reference to the trustee or the executor, administrator, heir or other legal representative having ownership or control over trust property.

Subsection 104(1) currently provides that, except for the purposes of certain specified provisions, references in the Act to trusts are considered not to include an arrangement where a trust can reasonably be considered to act as agent for its beneficiaries with respect to all dealings in all of the trust's property. These arrangements are generally known as "bare trusts". Trusts described in paragraphs (a) to (e.1) of the definition "trust" in subsection 108(1) are expressly not affected by this exclusion. Subsection 104(1) currently provides that the exclusion for bare trusts does not apply for the purposes of section 150. As such, these trusts are generally required to file an annual trust return and are subject to the beneficial ownership reporting requirements set out in section 204.2 of the Income Tax Regulations.

Subsection 150(1.3) also provides that for the purpose of section 150 a trust includes an arrangement under which a trust can reasonably be considered to act as agent for all the beneficiaries under the trust with respect to all dealings with all of the trust's property.

Subsection 150(1.3) is being amended to more clearly define the beneficial ownership arrangements that are subject to the reporting rules. This subsection will, subject to the exceptions in subsection 150(1.31), deem certain beneficial ownership arrangements that would not otherwise constitute a trust for the purposes of the Act to be a trust for the purposes of the beneficial ownership reporting rules.

Subsection 104(1) is amended to remove the reference to section 150. As such, beneficial ownership arrangements that are not otherwise treated as trusts for the purposes of the Act will only be subject to the beneficial ownership reporting requirements if they are deemed to be trusts under new subsection 150(1.3). This amendment will apply for taxation years that end after December 30, 2024.

Clause 13

Application of paragraph (1)(a)

ITA

107.4(2)(b)

Paragraph 107.4(2)(b) deems there to be no change in beneficial ownership of a property where the property is transferred from a trust governed by an RRSP or RRIF to another trust governed by an RRSP or RRIF, provided that the annuitant of the transferor is the same as that of the transferee.

Since property may be transferred from an RRSP to an FHSA of an individual (see paragraph 146(16)(a.2)), or from an individual's FHSA to an RRSP or RRIF under which the individual is the annuitant (see subsection 146.6(7)), or between FHSAs of the same individual, paragraph 107.4(2)(b) is amended to refer to trusts governed by an FHSA.

This amendment comes into force on April 1, 2023.

Clause 14

Employee options

ITA

110(1)(d)(i)(B)

Paragraph 110(1)(d) provides for a deduction in computing taxable income if certain conditions are met. The deduction is currently equal to half (proposed to be changed to one third consequential on proposed changes to the capital gains inclusion rate) of the amount of the benefit deemed by subsection 7(1) to have been received by a taxpayer in respect of a security under an employee stock option agreement.

Paragraph 110(1)(d) permits a deduction in computing taxable income of a deceased taxpayer who is deemed by subsection 7(1)(e) to have received a benefit in respect of a security because, immediately before death, the taxpayer owned a right to acquire the security under an employee stock option agreement. Under clause 110(1)(d)(i)(B), the deduction is available in these circumstances if (among other conditions) the security is acquired under the agreement within the first taxation year of the graduated rate estate of the taxpayer by:

- the graduated rate estate of the taxpayer,

- a person who is a beneficiary (as defined in subsection 108(1)) under the graduated rate estate of the taxpayer, or

- a person in whom the rights of the taxpayer under the agreement have vested as a result of the taxpayer's death.

Clause 110(1)(d)(i)(B) is amended consequential to changes to subsection 164(6.1) which provides the graduated rate estate of a deceased individual an additional two taxation years to carry back certain amounts related to rights to acquire securities held by the individual immediately before their death (as determined under subsection 164(6.1)) to be deducted in computing the deceased individual's income for their last taxation year.

For more information, see the commentary on subsection 164(6.1).

This amendment applies to taxation years of individuals who die on or after Announcement Date.

Annual vesting limit

ITA

110(1.31)

Subsection 110(1.31) applies to securities sold or issued by a qualifying person under a stock option agreement if the conditions in subsection 110(1.3) are met in respect of that agreement. It provides a formula for calculating the proportion of securities that are deemed to be non-qualified securities.

Subsection 110(1.31) is amended in two ways. First, the preamble is amended to clarify that the annual vesting limit formula, which deems a proportion of securities to be sold or issued under an agreement to be non-qualified securities, applies only in respect of those securities that could give rise to a deduction under paragraph 110(1)(d) (such securities being referred to as "specified securities" throughout the subsection). Other compensation arrangements that would not give rise to a paragraph 110(1)(d) deduction are not intended to count against the annual vesting limit.

Paragraph (b) under Variable D is amended to remove subparagraph (i), referring to securities that have been designated under subsection 110(1.4) as non-qualified securities (such securities cannot give rise to a deduction under paragraph 110(1)(d)). Similarly, clause (B) is removed. Narrowing the application of subsection (1.31) to only specified securities renders these two exclusions from paragraph (b) irrelevant.

Example

For example, assume Nathalie has entered into two equity-based compensation arrangements with her employer sequentially. The first agreement issues $400,000 worth of employee stock options (referring to the value of the underlying securities) and $250,000 worth of restricted share awards (meaning a right to acquire shares, on future vesting of the award, for a nil or nominal strike price). The second agreement issues $300,000 worth of employee stock options (referring to the value of the underlying securities) and $250,000 worth of restricted share awards. To demonstrate the effect of the amendment, assume all vest in the employee in the same year.

The table below illustrates how the formula in subsection 110(1.31) works pre- and post-amendment.

| Pre-Amendment | ||

|---|---|---|

| s. 110(1.31) | Agreement #1 | Agreement #2 |

| A | C + D - $200,000 = $450,000 | C + D - $200,000 = $450,000 |

| B | $650,000 | $450,000 |

| C | $650,000 | $450,000 |

| D | $0 | $200,000 |

| Result (A ÷ B) | $450,000/$650,000 = 69% of agreement #1 securities deemed non-qualified | $450,000/$450,000 = 100% of agreement #2 securities deemed non-qualified |

| Post-Amendment | ||

| s. 110(1.31) | Agreement #1 | Agreement #2 |

| A | C + D - $200,000 = $200,000 | C + D - $200,000 = $300,000 |

| B | $400,000 | $300,000 |

| C | $400,000 | $300,000 |

| D | $0 | $200,000 |

| Result (A ÷ B) | $200,000/$400,000 = 50% of agreement #1 securities deemed non-qualified | $300,000/$300,000 = 100% of agreement #2 securities deemed non-qualified |

In the absence of the amendment, the formula unintentionally counts Nathalie's restricted share awards against her annual vesting limit. The amendment ensures that the intended outcome, i.e., that $200,000 worth of stock options vesting in the same year are qualified (and therefore eligible for the employee stock option deduction), and that the remaining $500,000 worth of stock options are deemed non-qualified.

This amendment applies to agreements to sell or issue securities entered into after June 2021. However, it does not apply in respect of rights under an agreement to which subsection 7(1.4) of the Act applies that are new options in respect of which an exchanged option was issued before July 2021. This application date is retroactive to when the limitation in subsection 110(1.31) first began to apply.

Clause 15

Definitions

ITA

110.6(1)

"qualified small business corporation share"

This definition is relevant for the purposes of the capital gains exemption as only shares that constitute qualified small business corporation shares can qualify for the exemption.

The French version of paragraph (d) of the definition is amended to better align the English and French versions.

Clause 16

Loss on share held by trust

ITA

112(3.2)(a)(iii)

Subsection 112(3.2) provides a "stop-loss" rule that applies to reduce the loss of a trust (other than a mutual fund trust) on the disposition of a share of the capital stock of a corporation that was held by the trust as capital property.

Paragraph 112(3.2)(a) provides that the trust's loss otherwise determined on the disposition of the share is reduced by certain dividends received by the trust on the share. However, subparagraph 112(3.2)(a)(iii) limits this reduction in the case where the trust is an individual's graduated rate estate, the share was acquired as a consequence of the individual's death and the disposition occurs in the first taxation year of the estate. In this case, the loss reduction is reduced by half (proposed to be changed to one third consequential on proposed changes to the capital gains inclusion rate) of the lesser of the loss otherwise determined and the individual's capital gain from the disposition of the share immediately before the individual's death.

Subparagraph 112(3.2)(a)(iii) is amended consequential to changes to paragraph 164(6) which provide the graduated rate estate of a deceased individual an additional two taxation years to elect to treat certain capital losses and terminal losses of the taxpayer's estate as losses of the taxpayer for the taxpayer's last taxation year.

For more information, see the commentary on subsection 164(6).

This amendment applies to taxation years of graduated rate estates of individuals who die on or after Announcement Date.

Clause 17

Non-resident persons — 2010 Olympic and Paralympic Winter Games

ITA

115(2.3)

Subsection 115(2.3) exempts from taxable income amounts paid to certain non-resident persons in respect of activities performed in connection with the 2010 Olympic Winter Games or the 2010 Paralympic Winter Games.

As this provision is no longer relevant, it is repealed.

Clause 18

Annual adjustment

ITA

117.1(1)

Subsection 117.1(1) provides for the indexing of various amounts in the Act, based on annual increases to the Consumer Price Index.

The French version of subsection 117.1(1) is amended to better align the English and French versions.

Clause 19

Definitions

ITA

118(7)

"pension income"

Subparagraph (a)(iii.1) of the definition "revenu de pension" in the French version of the Act is amended to better align the French and the English versions of these subparagraphs. More specifically, a reference to "périodique" is deleted from the French version.

Clause 20

Definitions

ITA

120.4(1)

"excluded amount"

The definition "excluded amount" in subsection 120.4(1) describes income that is excluded from split income of an individual.

Paragraph (a) excludes from split income amounts derived from property that is inherited by an individual who has not attained the age of 24 years before the year from a parent, or from any other person if certain additional conditions are met.

Paragraph (b) excludes from split income amounts derived from property that is acquired by an individual under a transfer described in subsection 160(4). As a result, where a taxpayer transfers property to the taxpayer's spouse or common-law partner pursuant to a decree, order or judgment of a competent tribunal or a written separation agreement and, at that time, the taxpayer and spouse or common law partner were separated and living apart as a result of the breakdown of their marriage or common-law partnership, the income derived by the spouse or common-law partner from the property will be an excluded amount in respect of the spouse or common-law partner.

Paragraphs (a) and (b) are amended to ensure that an amount of income or taxable capital gain or profit, as the case may be, continues to qualify as an "excluded amount" where a property described in paragraph (a) or (b) is substituted for another property.

This amendment comes into force on Announcement Date.

Clause 21

Training amount limit

ITA

122.91(2)(a)(i)

Subsection 122.91(2) provides for the calculation of an individual's "training amount limit" for a taxation year for the purposes of the Canada Training Credit in subsection (1).

Subparagraph (a)(i) provides that an individual's training amount limit increases every year by $250, provided certain conditions are met, including that the total of certain specified amounts be equal to or exceed $10,000 in respect of the preceding taxation year. These specified amounts include certain amounts payable to the individual under the Employment Insurance Act.

Consequential to the enactment of new subsections 22.1(1) and 152.041(1) of the Employment Insurance Act relating to a new adoption benefit, subparagraph (a)(i) is amended to include references to these new provisions in sub-subclause (A)(III)2 of the description of B, applicable on the same date that these new provisions come into force.

Clause 22

Former resident — reassessment period

ITA

126(2.211)

Subsection 126(2.21) provides limited credits against an individual's Canadian tax that arises in the year of the individual's departure from Canada, for post-departure foreign taxes.

New subsection 126(2.211) provides that the Minister may make any assessment, reassessment or additional assessment in respect of the year of the individual's departure from Canada to take into account a deduction under subsection (2.21). This new subsection will ensure that the Minister may take into account this deduction where the period of time between the individual's departure from Canada and the moment when the foreign taxes arise is such that the Minister would otherwise have been prevented from doing so because of subparagraph 152(4)(b)(i).

Clause 23

Deemed rebate in respect of fuel charges

ITA

127.42(10)

New subsection 127.42(10) confirms that amounts paid under this section are deemed to have been paid as rebates in respect of charges levied under Part 1 of the Greenhouse Gas Pollution Pricing Act.

Clause 24

Adjusted taxable income determined

ITA

127.52(1)(d.1)

Paragraph 38(a.1) provides that the taxable capital gains inclusion rate is 0% on the donation of publicly listed securities to qualified donees. Paragraph 125.52(1)(d.1) provides that the taxable capital gains inclusion rate on the donation of publicly listed securities will be 3/10 (or 30%) for the purposes of computing an individual's minimum tax.

Paragraph 125.52(1)(d.1) is amended to provide that this paragraph would not apply to donations of a flow-through class of property (as defined in section 54). As such, donations of a flow-through class of property would not be subject to the AMT. Donations of a flow-through share class of property are addressed in new paragraph 127.52(1)(d.2).

This amendment applies to taxation years that begin after 2023.

ITA

127.52(1)(d.2)

This amendment adds new paragraph 127.52(1)(d.2). This amendment provides that the taxable capital gains inclusion rate on the donation of publicly listed securities will be 3/10 (or 30%) for the purposes of computing an individual's minimum tax of the capital gain that is the "true" capital gain from the disposition of a flow-through share class of property.

This amendment applies to taxation years that begin after 2023.

ITA

127.52(1)(e) and (e.1)

Paragraph 127.52(1)(e) provides that "adjusted taxable income" is computed on the assumption that the total of specified resource-related deductions does not exceed specified resource income. Paragraph 127.52(1)(e.1) provides that "adjusted taxable income" is computed on the assumption that financing expenses deductible under paragraphs 20(1)(c) to (f) in respect of the acquisition of flow-through shares, Canadian resource properties or foreign resource properties do not exceed the amount by which the same specified resource income exceeds the same specified resource-related deductions.

These paragraphs are repealed.

This amendment applies to taxation years that begin after 2023.

ITA

127.52(1)(j)

Paragraph 152(1)(j) limits certain deductions to a rate of 50% for the purposes of computing an individual's minimum tax.

Subparagraph 125.52(1)(j)(ii) provides that for the purposes of computing an individual's minimum tax, the individual may only deduct one half of the amounts otherwise deducted in the year for interest and financing expenses in respect of an amount borrowed to earn income from property. This limitation does not apply for the purposes of other provisions of the minimum tax rules that apply to limit the deduction of interest and financing expenses for specific purposes. The limitation also does not apply to money borrowed by an employee ownership trust (or a Canadian-controlled private corporation that is controlled and wholly-owned by the trust) to acquire a qualifying business pursuant to a qualifying business transfer.

Paragraph 127.52(1)(j)(ii) is amended to provide that this 50% limitation on the deduction of expenses also applies to amounts deducted under paragraph 20(1)(bb) (fees paid to investment counsel).

This amendment applies to taxation years that begin after 2023.

Clause 25

Post-emigration loss — reassessment period

ITA

128.1(8.1)

Subsection 128.1(8) provides relief to an individual (other than a trust) who disposes of a taxable Canadian property, after having emigrated from Canada, for proceeds that are less than the deemed proceeds that arose under paragraph 128.1(4)(b) in respect of the property when the individual emigrated. Under subsection 128.1(8) the individual may elect to reduce the proceeds of disposition that were deemed to arise under paragraph 128.1(4)(b) in respect of a property by the least of certain specified amounts.

New subsection 128.1(8.1) provides that the Minister may make any assessment, reassessment or additional assessment in respect of the year in which the proceeds of disposition were deemed to arise to take into account an election to reduce those proceeds under subsection (8). This new subsection will ensure that the Minister may take into account the election where the period of time between the moment when the proceeds of disposition were deemed to arise and the moment when the property is subsequently disposed of is such that the Minister would otherwise have been prevented from doing so because of subparagraph 152(4)(b)(i).

Clause 26

Acceptance of plan for registration

ITA

146(2)

Subsection 146(2) of the Act sets out the conditions that a registered retirement savings plan must comply with in order to be registered with the Canada Revenue Agency.

That subsection is amended to add a requirement that an application for registration be made in a prescribed manner. See additional commentary for the amendment to the definition "prescribed" in subsection 248(1) of the Act.

This amendment comes into force on royal assent.

Transfer of funds

ITA

146(16)(b)

Subsection 146(16) allows taxpayers to transfer funds on a tax-deferred basis from their registered retirement savings plan (RRSP) to registered vehicles listed in that subsection before maturity of the transferor RRSP.

Paragraph 146(16)(b) is amended to allow for a transfer from an RRSP to a registered pension plan for the benefit of a spouse or common-law partner or former spouse or common-law partner as a result of a division of property on the breakdown of marriage or common-law partnership. In addition, the requirement for "living separate and apart" is deleted.

This amendment comes into force on royal assent.

Clause 27

Acceptance of fund for registration

ITA

146.3(2)

Subsection 146.3(2) of the Act sets out the conditions that a registered retirement income fund must comply with in order to be registered with the Canada Revenue Agency.

That subsection is amended to add a requirement that an application for registration be made in a prescribed manner. See additional commentary for the amendment to the definition "prescribed" in subsection 248(1) of the Act.

This amendment comes into force on royal assent.

Transfer on breakdown of marriage or common-law partnership

ITA

146.3(14)

Subsection 146.3(14) provides for the direct transfer (i.e., tax deferred) of an amount from an annuitant's RRIF to an RRSP or RRIF of the annuitant's current or former spouse or common-law partner on the breakdown of their marriage or common-law partnership.

Paragraph 146.3(14)(b) is amended by adding a subparagraph (ii) to include registered pension plans in the list of vehicles available for a direct transfer from a RRIF for the benefit of the annuitant's current or former spouse or common-law partner after the relationship breakdown.

This amendment comes into force on royal assent.

Clause 28

Definitions

ITA

146.5(1)

"advanced life deferred annuity"

The definition "advanced life deferred annuity" (ALDA) in subsection 146.5(1) of the Act provides the conditions that an annuity contract must meet to qualify as an ALDA contract.

Amendments to subsections 146.5(1), (4.1) and (5) of the Act are being made to better align the ALDA tax rules with various provincial pension standards laws that apply to annuities purchased from registered plans.

Subparagraph 146.5(1)(c)(ii) is amended to add a reference to a former spouse or common-law partner of the annuitant to allow for the annuity to be payable for the joint life of the annuitant and their former spouse or partner, consistent with provincial legislation.

Subparagraph 146.5(1)(d)(ii) is amended to allow the amount of the annuity to be changed to allow sharing of rights between spouses or common-law partners after the breakdown of a marriage or a partnership. It is also amended to allow for an annuity to be adjusted on an actuarially equivalent basis if a spouse or common-law partner is no longer entitled to the annuity.

Paragraph (f) of the definition describes the sole type of lump sum death benefit payable from an ALDA. Subparagraph (f)(ii) is amended to allow the death benefit to be computed with interest at a rate specified under pension benefit standards legislation.

New paragraph (g.1) is added to the definition to allow for the payment under the contract to a spouse or common-law partner (or former spouse or common-law partner) on or after the breakdown of their marriage or common-law partnership in settlement of rights from their marriage or partnership as a single amount, periodic payment or a direct transfer to an RRSP, RRIF, pooled registered pension plan or a money purchase provision of a registered pension plan.

Paragraph (i) of the definition requires the annuity contract to stipulate that no right under the contract is capable of being assigned, charged, anticipated, given as security or surrendered. Paragraph (i) is amended to provide an exception for amounts required to be paid as a result of the breakdown of marriage as described in new paragraph (g.1) or support payments made under a judicial order or a written agreement.

These amendments are deemed to come into force on January 1, 2023.

Taxable amount – marriage breakdown

ITA

146.5(4.1)

New subsection 146.5(4.1) is added to the Act to require that amounts paid under paragraph (g.1) of the definition of "advanced life deferred annuity" (in subsection 146.5(1)) be included in the income of the recipient spouse or common-law partner (or former spouse or common-law partner), unless subsection 146.5(5) applies.

This amendment is deemed to come into force on January 1, 2023.

Treatment of amount transferred

ITA

146.5(5)

Subsection 146.5(5) of the Act contains rules that apply to an amount refunded from an ALDA that is transferred directly to a registered vehicle.

Subsection 146.5(5) is amended, consequential to paragraph (g.1) of the definition of "advanced life deferred annuity" (in subsection 146.5(1)), so that these rules will also apply to the transfers described in subparagraph (g.1)(ii)(C).

This amendment is deemed to come into force on January 1, 2023.

Clause 29

Definitions

ITA

146.6(1)

"annual FHSA limit"

The definition "annual FHSA limit" is used in the determination of the amount an individual may deduct under subsection 146.6(5), in respect of contributions to a FHSA, in computing the individual's income for a particular taxation year. The annual FHSA limit for a particular taxation year is the lesser of paragraphs (a), (b) and (c) of the definition.

The definition is amended to ensure that designated withdrawals made after a qualifying withdrawal do not unintentionally result in disallowance of deductions for contributions made prior to the qualifying withdrawal. In particular, variable C in paragraph (a) of the definition is amended to exclude amounts designated after the taxpayer's first qualifying withdrawal from the total of all designated amounts described in paragraph (b) of the definition designated amount in subsection 207.01(1) for the year.

This amendment comes into force on April 1, 2023.

Deemed transfer or distribution

ITA

146.6(15)

Subsection 146.6(15) of the Act deals with situations in which an amount paid from a deceased holder's FHSA to the holder's estate would have been eligible for a tax-free transfer under subsection 146.6(7) to a survivor (spouse or common-law partner), or would have been taxable to a beneficiary if the amount had been paid directly to the beneficiary from the FHSA, to the extent that the recipient has a beneficial interest under the deceased holder's estate.

Paragraph 146.6(15)(a) allows the legal representative of a deceased holder's estate and the survivor to jointly designate (via a prescribed form) to have the FHSA proceeds that were paid to the estate treated as having been transferred from the FHSA of the deceased holder to an FHSA, RRSP or RRIF of the survivor.

In the same vein as the recently amended subsection 146(8.1), this amendment will permit a joint designation to be filed in cases where a spouse or common-law partner is neither a successor holder nor a beneficiary of the FHSA or the estate of the deceased FHSA holder, but where a payment is made from the estate to a surviving spouse or common-law partner in accordance with a court order or written agreement relating to rights or interests in respect of the property from a marriage or common-law partnership. Furthermore, the words "in full or partial satisfaction of the survivor's rights" are removed, as they are unnecessary for the interpretation and application of the provision.

This amendment comes into force on April 1, 2023.

Clause 30

Definitions

ITA

147(1)

"deferred profit sharing plan"

Subsection 147(1) defines terms used in the provisions relating to deferred profit sharing plans (DPSPs).

The definition of "deferred profit sharing plan" is amended to remove the requirement that both the trustee under the plan and an employer of employees who are beneficiaries under the plan apply in prescribed manner for registration. The new requirement is that either the trustee under the plan or a participating employer may apply in prescribed manner for registration.

This amendment comes into force on royal assent.

Clause 31

Notice of revocation

ITA

147.1(12)

Subsection 147.1(12) provides that, after the Minister of National Revenue has given a notice of intention to revoke the registration of a pension plan, the Minister may give a further notice that the registration of the plan is revoked as of a specified date, which date may be no earlier than the date stated in the notice of intent. Subsection 147.1(12) also allows the Minister to give a notice of revocation where a plan administrator applies for the revocation of plan registration.

Subsection 147.1(12) is amended to clarify that the date of revocation in an administrator's application to revoke a plan's registration only applies in the case where the Minister of National Revenue has not given a notice of intention to revoke. That is, if the Minister had issued a notice of intention, the date of revocation specified by the Minister will prevail over any other date requested by the plan administrator.

This amendment comes into force on royal assent.

Clause 32

Commutation of annuity contract

ITA

147.4(4) and (5)

Where an individual acquires ownership of an annuity in satisfaction of the individual's entitlement to benefits under a registered pension plan (RPP) and certain other conditions are met, subsection 147.4(1) deems the individual not to have received an amount from the RPP as a result of acquiring the annuity and deems amounts received under the contract to be amounts received under the RPP. As a consequence, there is no immediate taxation on acquisition of the annuity and any payments under the contract are included in the recipient's income in the year in which they are received.

The Act currently prohibits the value of the annuity from being transferred to a registered vehicle of the annuitant. Section 147.4 is amended by adding subsections (4) and (5) to allow for a transfer of the commuted value of the annuity in certain circumstances.

Subsection 147.4(4) sets out the situations in which an annuity contract may be commuted and transferred on a tax-deferred basis, including if

- a spouse or common-law partner or former spouse or common-law partner is entitled to a portion of the annuity in settlement of rights on the breakdown of marriage or common-law partnership,

- in the case of an annuity that had been purchased on behalf of an individual consequential to proceedings commenced under the Bankruptcy and Insolvency Act or the Companies' Creditors Arrangement Act, the individual subsequently decides, before annuity payments commence, to surrender the annuity and receive its commuted value,or

- the Pension Benefits Standards Act, or similar law of a province permits the annuitant to commute or surrender the annuity.

Subsection 147.4(5) sets out the registered vehicles where the commuted value may be transferred, if the conditions in new subsection 147.4(4) are met. The commuted value may be transferred to a money purchase provision of an RPP, registered retirement savings plan or registered retirement income fund of the annuitant (or the spouse or common-law partner or former spouse or common-law partner of the annuitant).

In the case of an interest in the annuity contract that was acquired as a consequence of a transfer of property from a defined benefit provision of a pension plan, the amount transferred may not exceed the prescribed amount described in paragraph 147.3(4)(c) to be transferred to a money purchase provision of a registered pension plan, registered retirement savings plan or registered retirement income fund.

This amendment comes into force on January 1, 2018.

Clause 33

Exclusions

ITA

149.1(1.1)

Subsection 149.1(1.1) of the Act excludes certain amounts from being included in determining if a registered charity has satisfied its annual disbursement quota.

Existing paragraph 149.1(1.1)(d) provides that expenditures on administration and management of the charity shall not be considered to have been expended on charitable activities carried on by the organization for the purposes of satisfying its disbursement quota.

Paragraph 149.1(1.1)(d) is amended to add a reference to fundraising. This clarifies that expenditures on fundraising do not count towards satisfying an organization's disbursement quote.

Whether a particular expenditure relates to administration, management and fundraising will be a factual determination based on the activities and practices of the organization.

This amendment comes into force on royal assent.

Clause 34

Exception

ITA

150(1.1)(a)

Subsection 150(1) stipulates the tax return requirements and the filing dates for different categories of taxpayers. Subsection 150(1.1) sets out exceptions to subsection 150(1), when the filing of a tax return is not required.

Currently, paragraph 150(1.1)(a) only exempts a registered charity from the filing requirements under subsection 150(1) if it is also a corporation.

Paragraph 150(1.1)(a) is amended to exempt from the filing requirements under subsection 150(1) any taxpayer who was a registered charity throughout the year.

Exception - trusts

ITA

150(1.2)(b)

Subsection 150(1) stipulates the tax return requirements and the filing dates for different categories of taxpayers. Subsection 150(1.1) sets out exceptions to subsection 150(1), when the filing of a tax return is not required. Subsection 150(1.2) provides that subsection 150(1.1) does not apply in respect of an express trust, unless it meets one of the exceptions listed in paragraphs 150(1.2)(a) to (p).

In addition, a trust that is required to file a return under subsection 150(1) is not required to provide the additional information set out in section 204.2 of the Regulations if it meets one of the exceptions listed in paragraphs 150(1.2)(a) to (p). As such, trusts that are required to file a return, and that do not meet one of these exceptions, will be required to provide the additional information outlined in section 204.2 of the Regulations.

Several amendments are being made to add or broaden exceptions in subsection 150(1.2).

Paragraph 150(1.2)(b) provides that the beneficial ownership reporting requirement does not apply in respect of a trust if the trust hold assets with a total fair market value that does not exceed $50,000 throughout the year, where the only assets held by the trust throughout the year are one or more of:

- money,

- certain government debt obligations,

- a share, debt obligation or right listed on a designated stock exchange,

- a share of the capital stock of a mutual fund corporation,

- a unit of a mutual fund trust,

- an interest in a related segregated fund (within the meaning assigned by paragraph 138.1(1)(a), and

- an interest, as a beneficiary under a trust, that is listed on a designated stock exchange.

Paragraph 150(1.2)(b) is amended to remove the requirement that the assets of the trust constitute the specific assets currently prescribed in that paragraph.

New paragraph 150(1.2)(b.1) provides an expanded relieving exception where each beneficiary of the trust is an individual and related to each trustee of the trust. This new exception would apply where:

- each trustee is an individual, and

- the total fair market value of the property of the trust does not exceed $250,000 throughout the year and the only assets held by the trust throughout the year are one or more of

- money,

- a guaranteed investment certificate issued by a Canadian bank or trust company incorporated under the laws of Canada or of a province,

- a debt obligation described in paragraph (a) of the definition fully exempt interest in subsection 212(3),

- debt obligations issued by

- a corporation, mutual fund trust or limited partnership the shares or units of which are listed on a designated stock exchange in Canada,

- a corporation the shares of which are listed on a designated stock exchange outside Canada, or

- an authorized foreign bank that are payable at a branch in Canada of the bank,

- a share, debt obligation or right listed on a designated stock exchange,

- a share of the capital stock of a mutual fund corporation,

- a unit of a mutual fund trust,

- an interest in a related segregated fund trust (within the meaning assigned by paragraph 138.1(1)(a)),

- an interest as a beneficiary under a trust, all the units of which are listed on a designated stock exchange,

- personal use property of the trust, or

- a right to receive income on property described above.

Paragraph 150(1.2)(c) provides an exemption to the beneficial ownership reporting requirements for trusts that are required under the relevant rules of professional conduct or the laws of Canada or a province to hold funds for the purposes of the activity that is regulated under those rules or laws, provided the trust is not maintained as a separate trust for a particular client or clients (this provides an exception for a professional's general trust account, but not for specific client accounts).

Paragraph 150(1.2)(c) is amended to extend this exception to specific accounts provided the only assets held by the trust throughout the year are money with a value that does not exceed $250,000.

New paragraph 150(1.2)(q) provides, for greater certainty, that the limitation in this subsection would not apply to statutorily created trust relationships, such as those of bankruptcy trustees or provincial guardians.

This amendment applies to taxation years that end after December 30, 2024.

Deemed trust

ITA

150(1.3)

Subsection 150(1.3) currently provides that, for the purposes of section 150, trusts include an arrangement where a trust can reasonably be considered to act as agent for its beneficiaries with respect to all dealings in all of the trust's property. These arrangements are generally known as "bare trusts". This, along with current subsection 104(1), mean that bare trusts are currently subject to the reporting requirements in this section and section 204.2 of the Regulations.

Existing subsection 150(1.3) is repealed. This, along with the amendment to remove the reference to section 150 in subsection 104(1), means that beneficial ownership arrangements that are not otherwise treated as trusts for the purposes of the Act will only be subject to the beneficial ownership reporting requirements if they are deemed to be trusts under new subsection 150(1.3).

The amendment to repeal subsection 150(1.3) applies to taxation years that end after December 30, 2024. This means that "bare trusts" will not be required to file returns for taxations years ending on December 31, 2024.

Subsection 150(1.3) is replaced with new wording to provide greater certainty and to effectively define what constitutes a "bare trust" for the purposes of the beneficial ownership reporting requirements. This new subsection relies upon the existing trust concept of the division of legal and beneficial ownership and is intended, subject to the exceptions in subsection 150(1.31), to capture those arrangements that would normally constitute a bare trust. This change, together with the exceptions in new 150(1.31), is intended to provide more clarity on the arrangements that are subject to the reporting rules.

New subsection 150(1.3) provides that for the purposes of section 150 and section 204.2 of the Regulations:

- a trust is deemed to include any arrangement under which

- one or more persons (the legal owner) have legal ownership of property that is held for the use of, or benefit of, one or more persons or partnerships, and

- the legal owner can reasonably be considered to act as agent for the persons or partnerships who have the use of, or benefit of, the property;

- each person that is a legal owner of an arrangement set out above is deemed to be a trustee of the trust; and

- each person or partnership that has the use or benefit of property under an arrangement that is set out above is deemed to be a beneficiary of the trust.

Subsection 150(1.31) provides that subsection 150(1.3) does not apply to an arrangement that meets one of the exceptions listed in paragraphs 150(1.31)(a) to (g).

Subject to the exemptions in subsection 150(1.2), if subsection 150(1.3) deems an arrangement to be a trust in a year, beneficial ownership information of that trust would be required to be reported to the CRA for that year.

The amendment to add the new version of subsection 150(1.3) applies to taxation years that end after December 30, 2025. Accordingly, it would first be applicable to taxation years that end on December 31, 2025. This is intended to allow taxpayers and their advisors sufficient time to consider their circumstances in light of new subsections 150(1.3) and (1.31) (discussed below).

ITA

150(1.31)

New subsection 150(1.31) provides that subsection 150(1.3) does not apply to an arrangement that meets one of the exceptions listed in paragraphs (a) to (g).

New subsection 150(1.31) provides that subsection 150(1.3) does not apply to an arrangement for a taxation year if:

- Each person or partnership that is deemed to be a beneficiary by subsection (1.3) at any time in the year is also a legal owner of the property referred to in that paragraph at that time and there are no legal owners that are not deemed to be beneficiaries. This would provide certainty that subsection 150(1.3) would not apply in circumstances where individuals hold the property both for their own use and benefit and for that of another person, such as where family members hold a joint bank account.

- The legal owners are individuals that are related persons and the property is real property that would be the principal residence of one or more of the legal owners for the year if those legal owners had designated the property for the year under the definition principal residence in section 54. This would exclude arrangements such as where a parent is on title to allow a child to obtain a mortgage.

- The legal owner is an individual and the property is real property that is held for the use of, or benefit of, the legal owner's spouse or common-law partner during the year and would be the legal owner's principal residence for the year if the legal owner had designated the property for the year under the definition principal residence in section 54. This would exclude circumstances where spouses jointly occupy a family home, but only one spouse is on title.

- Under the arrangement the property is held throughout the year solely for the use of, or benefit of, a partnership, each legal owner is a partner (other than a limited partner) of the partnership, and a member of the partnership is, or but for subsection 220(2.1) would be, required under section 229 of the Regulations to make an information return for a fiscal period of the partnership that includes December 31 of that year. This would exclude circumstances where a partner (other than a limited partner) holds property for the use or benefit of the partnership.

- The legal owner holds the property pursuant to an order of a court.

- An arrangement where Canadian resource property is held for the use or benefit of one or more publicly listed companies (or subsidiaries or partnerships of such companies).

- An arrangement where a non-profit organization holds funds it has received from the federal or provincial governments for the use or benefit of other non-profit organizations.

This amendment applies to taxation years that end after December 30, 2025.

Clause 35

Assessment

ITA

152(1)(b)

Paragraph Section 152 sets out the provisions relating to assessments. Paragraph 152(1)(b) requires the Minister of National Revenue, in assessing tax for a year, to make a determination of the amount of tax that is deemed to have been paid by a taxpayer under certain provisions of the Act. In the absence of such a determination, a taxpayer would not be entitled to object or appeal in respect of such amounts.

Paragraph 152(1)(b) is amended to add references to subsection 122.92(3) (the multigenerational home renovation tax credit), subsections 127.42(2) and (3) (carbon tax refund to farmers) and subsections 122.421(2) and (3) (the Canada carbon rebate).

This amendment comes into force on June 20, 2024.

Provisions applicable

ITA

152(1.2)(d)

Paragraph 152(1.2)(d) is currently relevant for purposes of the GST/HST Credit, the advance payments of the Canada workers benefit and the Climate Action Incentive under sections 122.5, 122.72 and 122.8, respectively. Paragraph 152(1.2)(d) provides that where the Minister determines the amount deemed by subsection 122.5(3) to (3.003), 122.72(1) or 122.8(4) to have been paid by an individual for a taxation year to be nil, the Minister is not required to send the individual a notice of determination unless the individual requests a notice of determination from the Minister.

Consequential on the introduction of new subsections 127.421(2) and (3) (which provide the Canada carbon rebate to qualifying corporations), paragraph 152(1.2)(d) is amended to provide that it also applies to a nil determination made to a person under new subsections 127.421(2) and (3).

This amendment comes into force on Royal Assent.

Reassessment with taxpayer's consent

ITA

152(4.2)(b)

Subsection 152(4.2) contains rules relating to the reassessment of tax, interest and penalties payable by a taxpayer and to the redetermination of tax deemed to have been paid by a taxpayer. This subsection gives the Minister of National Revenue discretion to make a reassessment or a redetermination beyond the normal reassessment period when so requested by an individual (other than a trust) or a graduated rate estate.

Paragraph 152(4.2)(b) is amended to add a reference to subsection 122.92(3) (the multigenerational home renovation tax credit).

This amendment applies as of January 1, 2023.

Reassessment where certain deductions claimed

ITA

152(6)

Consequential to the enactment of subsections 126(2.211) and 128.1(8.1), subsection 152(6) is amended by removing the reference to subsection 126(2.21) in paragraph (f.1) and by repealing paragraph (f.2).

Clause 36

Withholding

ITA

153(1)(b) and (b.1)

Section 153(1) requires the withholding of tax from certain payments described in paragraphs 153(1)(a) to (v). The person making such a payment is required to remit the amount withheld to the Receiver General on behalf of the payee. Paragraph (b) requires withholding with respect to a superannuation or pension benefit.

Consequential to the amendments to paragraph 56(1)(a) related to the timing of the income inclusion for unclaimed pension property, subsection 153(1) is amended to apply withholding requirements only when a claimant receives the amount from a designated entity (e.g. Bank of Canada in the case of federally regulation pension plans) that held the previously unclaimed property. See additional commentary for the amendment to paragraph 56(1)(a) of the Act.

This amendment comes into force on royal assent.

ITA

153(1)(g)

Paragraph 153(1)(g) is amended consequential on the repeal of subsection 115(2.3), to remove the reference to that subsection.

Clause 37

Where excess refunded

ITA

160.1(1)(b)

Subsection 160.1(1) provides for the recovery of an amount refunded to a taxpayer under the Act in excess of the amount to which the taxpayer was entitled. Paragraph (b) provides that interest is to be paid by the taxpayer on the excess amount recovered at the prescribed rate, except that no interest is to be paid on the portion of the excess amount that represents a repayment of the GST/HST credit (GSTC) under section 122.5, the Canada child benefit under section 122.61, the partial delivery of the Canada workers benefit through advance payments under section 122.72 or the climate action incentive under section 122.8.

Paragraph (b) is amended consequential on introduction of new section 127.421 to provide the Canada carbon rebate. Consistent with treatment of the GST/HST credit, Canada child benefit, Canada workers benefit and climate action incentive, paragraph (b) is amended to provide that no interest is charged on any excess portion of a refund that represents a repayment of the Canada carbon rebate payments paid to a taxpayer under section 127.421.

This amendment applies as of June 20, 2024.

Clause 38

Rules applicable

ITA

160.2(4)